Mantle - 0 To 1

The 0-to-1 Inflection Point

Mantle ($MNT) presents a compelling asymmetric opportunity as it transitions from a token loosely associated with Bybit to a utility-integrated, exchange-owned token—a genuine 0-to-1 moment. The investment thesis centers on MNT's positioning at a critical inflection point analogous to BNB's early utility integration with Binance, with several structural advantages that suggest significant revaluation potential.

Key Investment Drivers:

- ◆Sizeable opportunity at $10B FDV allowing for meaningful position allocation

- ◆Multiple converging catalysts creating structural demand drivers

- ◆Strong underlying business fundamentals with Bybit as the world's second-largest derivatives exchange

- ◆Strong leadership, led by Ben Zhou

- ◆Aligned tokenomic incentives with tokenholders

- ◆Permanent capital inflows through utility

- ◆Multiple narratable factors providing tailwinds as an easy story to tell

- ◆Favorable risk-reward profile at current valuation multiples

The market historically rewards explosive re-ratings when tokens transition from "exchange-related" to "exchange utility" status: BNB's trajectory from $15 to $690 following Binance integration and OKB's appreciation from $1 to $45 demonstrate this pattern. Mantle currently sits at this same structural inflection point, with comparable utility integration but at substantially lower valuation multiples.

- ◆Catalyst Analysis & Growth Dynamics

Source: Bybit

A). Immediate Catalysts

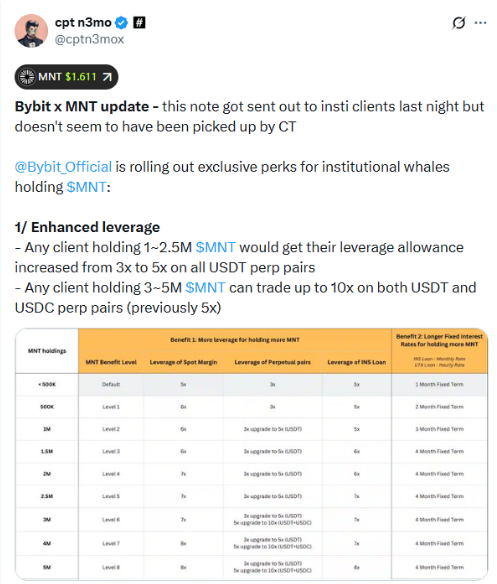

- ◆Enhanced Leverage for Institutions

- ◆Hold 1-2.5M MNT → increase leverage from 3x to 5x on USDT perpetuals

- ◆Hold 3-5M MNT → access 10x leverage on USDT/USDC perpetuals

- ◆Direct targeting of institutional traders requiring higher leverage strategies

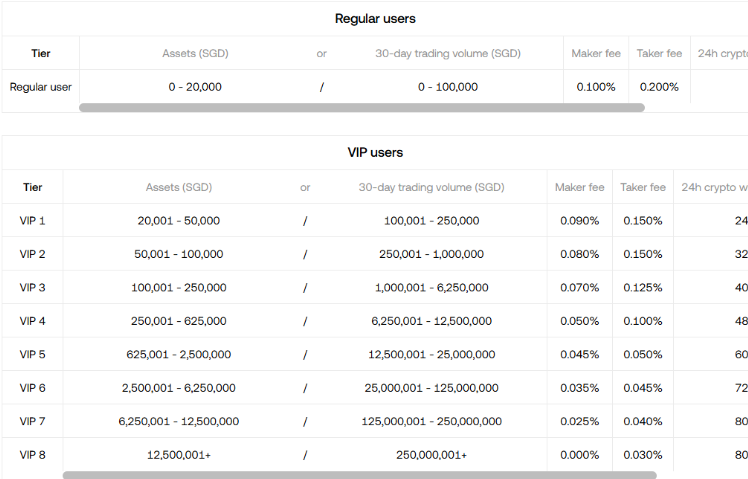

- ◆VIP Fee Discounts

- ◆25% discount on spot trading fees

- ◆10% discount on derivatives

- ◆Collateral Enhancement

- ◆MNT loan-to-value ratio increased from 10% to 60%—a 6x improvement reducing capital requirements for large traders

- ◆OTC Portal (Q4 Launch)

- ◆Direct institutional buying channel addressing current liquidity constraints

- ◆Autonomous bulk trading system targeting whale/fund segment accumulation needs

Demand Quantification

These are just some of the catalysts that converge to create substantial token demand. According to Emily (Head of Spot Business at Bybit and Key Advisor at Mantle), if 20-30% of VIP traders (representing 75-80% of volume) utilize fee discounts, this could result in 15-20% of Bybit's total volume being paid in MNT.

At Bybit's approximately $4 billion annual revenue, this represents potentially $500+ million in MNT token demand annually. This constitutes an evergreen demand driver unlike speculative narratives—fee discounts create permanent structural buying pressure, as evidenced by BNB's sustained performance.

High-frequency traders and institutions require these discounts daily across all trades. The cost savings represent a non-negotiable tool that pays for itself over time, creating consistent buying pressure.

B). Bybit's Exceptional Growth Profile

Mantle benefits from Bybit launching utility integration at a significantly larger scale than Binance achieved during BNB's initial activation. Bybit already operates as a top-3 global exchange, allowing MNT to bypass the "early adoption" phase and immediately access an established, massive user base of VIP traders requiring cost savings.

Growth Metrics

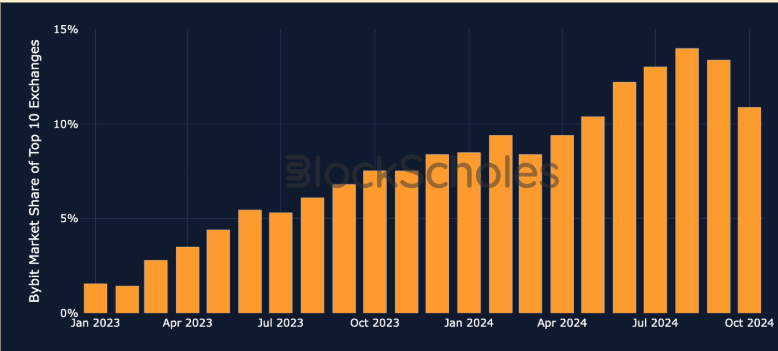

Figure 1. Bybit’s market share as a proportion of market share of the top 10 centralized exchanges, measured by trade volume. Source: Block Scholes

Market share explosion: 1.56% → 12.21% in 2 years (7x growth while competitors stagnated). By 2024, Bybit became the second-largest centralized crypto exchange by trading volume. It has exceeded the 10% mark, a testament to its growing success in capturing a larger volume of crypto traders.

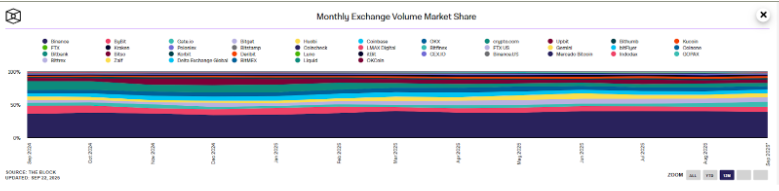

Figure 2. Bybit’s market share as a proportion of the market share of the top 10 centralized exchanges, measured by trade volume. Bybit is second place at 7.75%. Source: The Block

The same comparison holds across the top 10 exchanges by perpetual swap trading volume. It is #2 globally - with Binance at 38.76% of all monthly exchange volume, and Bybit in second place at 7.75%.

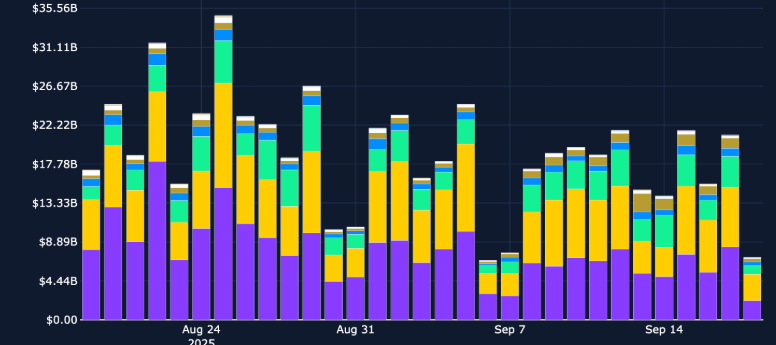

Source: Block Scholes

Lastly, Bybit consistently processes $4-13 billion in daily trading volume, with peaks reaching $35.5 billion during major market events.

Overall, Bybit is in a strong position. Geographic presence includes positioning in Russia (24% of traffic), Germany (6%), and growing Asian markets. This is reflected in their strong user growth - they grew from 20m users in late 2023, to 60m users in Q3 2024, and 70m registered users as of May 9, 2025. This provides the reach necessary to drive MNT adoption at scale.

C). Leadership and Crisis Management

Bybit's leadership team demonstrated exceptional capabilities during the February 2025 $1.5 billion Lazarus Group hack. CEO Ben Zhou's team displayed one of the strongest crisis management responses in crypto history - within 72 hours, they fully replenished client funds while maintaining 100%+ reserve ratios and operational continuity. The exchange's market share only temporarily dropped from 12% to 8% before recovering - a testament to user confidence in the leadership.

Given this proven leadership caliber, the appointment of Bybit Co-CEO Helen Liu and Head of Spot Trading Emily Bao as Key Advisors to Mantle in August 2025 during the latest Bybit x Mantle Live Recap carries significant strategic weight. When executives of this demonstrated competence commit resources at the highest levels, it signals a fundamental shift in strategic commitment towards Mantle.

Strategic Priorities Outlined:

- ◆Maximizing Bybit's platform resources for Mantle—fee deductions, trading pairs, loans, VIP benefits

- ◆Building efficient infrastructure for RWA tokenization—positioning Mantle for institutional-grade assets

- ◆Cross-chain expansion—attracting users and assets through ecosystem interconnection

D). Exchange Chain Dynamics

This strategic direction aligns with the emergence and growth of "exchange chains"—Base and Binance Smart Chain (BSC) have performed exceptionally over the past year. Exchange-owned chains have proven to be one of the most successful models in crypto—they combine the exchange's user base, liquidity, and brand trust with native blockchain utility. Base leveraged Coinbase's institutional credibility and user base to become a dominant L2, while BSC used Binance's trading volume and ecosystem to create sustainable on-chain activity.

Today, the exchange wars are intensifying: BNB represents BSC and Binance, and Base hints at launching a token. Mantle enters this competitive landscape with institutional-grade infrastructure. The recent acquisition of UR Bank, built on the Mantle chain, demonstrates commitment to bridging traditional banking with DeFi and building "the core hub for RWA on-chain." This creates what Helen Liu described as "a closed loop from asset on-chain - liquidity and product - user reach."

As such, the crucial difference with Bybit’s Mantle is that Bybit is entering this space with far more going for it. Bybit enters this space with MiCA compliance, established institutional relationships, and demonstrated growth momentum. This execution advantage, if realized effectively, should drive significant revaluation.

2. Narrative Alignment and Tokenomics

Mantle aligns with the strongest current narratives. The market is rewarding tokens that actually generate cash flows and have real business models behind them:

- ◆Launchpads

- ◆Perpetual DEXs

- ◆Exchange tokens

- ◆Layer 1s

- ◆Stablecoins

- ◆DeFi protocols

These represent the financial infrastructure crypto has developed over five years, with the market accepting financial services as crypto's primary use case rather than speculative narratives.

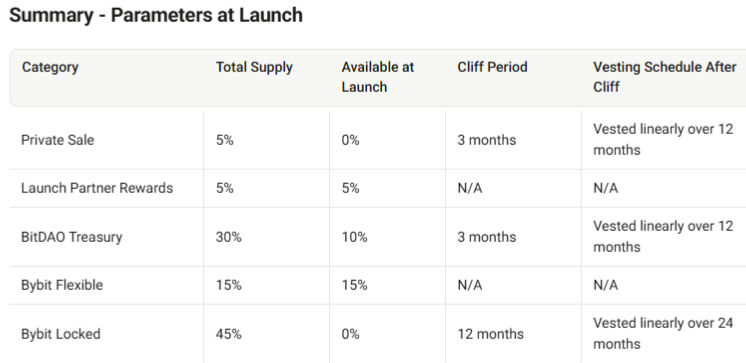

Supply Structure

Tokenomics wise, MNT's tokenomics reflect concentrated control, with approximately 90% of effective supply controlled by Bybit and affiliated entities. Public disclosures show 48% treasury holdings and 52% circulating supply, though historical BitDAO allocation data indicates:

- ◆45% Bybit Allocation

- ◆30% BitDAO Treasury

- ◆15% Bybit Flexible Allocation

Source: BitDao Docs

While this concentration may seem to represent huge governance liability - it is a structural advantage instead. Market evidence has thus far supported two different kind sustainable tokenomics models:

- ◆Fully diluted assets with completed distribution cycles where selling pressure has been absorbed

- ◆Strategically controlled tokens held by entities with non-transactional business models

Examples in the first category include tokens like Raydium and Aave, which have weathered their major unlock cycles. Mantle falls into the second category, creating superior incentive alignment, instead of being a traditionally VC-backed project that faces structural selling pressure due to fund lifecycles and LP return requirements.

Thus, Bybit operates under different constraints. As an exchange generating $4 billion annually in trading fees, token sales represent a fractional revenue opportunity that would undermine their primary business model. Bybit's success depends on MNT functioning as effective utility infrastructure - enabling fee discounts, serving as collateral, and driving institutional adoption. Each of these use cases requires price stability and appreciation, not liquidation.

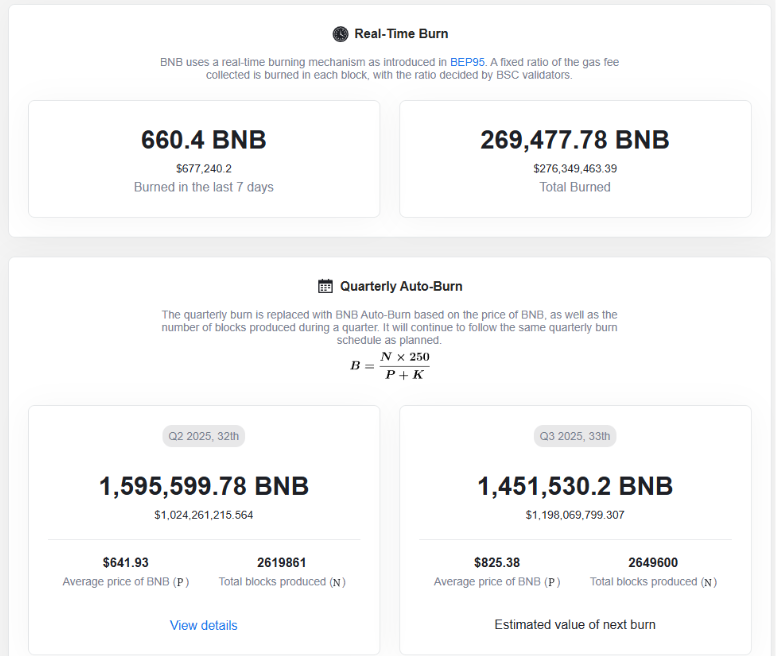

This alignment has proven successful historically. BNB demonstrates how exchange-controlled tokens can outperform when the parent entity has complementary business incentives. Binance maintains significant BNB holdings while focusing on token burns rather than sales, even recently burning over $1 billion worth of BNB in the past quarter. On top of that, the exchange's revenue model creates natural demand for BNB utility, supporting price appreciation that benefits both the exchange and token holders.

Source: BNBurn

OKX provides additional validation through OKB's dramatic supply reduction. In August 2024, OKX burned 279 million tokens worth $26 billion, reducing total supply by 93% to 21 million tokens. This deflationary event triggered a 200% price surge within hours, demonstrating the power of exchange-led tokenomics optimization.

With 90%+ control, exchanges can execute strategic initiatives without misaligned stakeholder interference. This concentration enables rapid decision-making and strategic flexibility that distributed governance models cannot match. Rather than representing risk, concentrated exchange control creates alignment between token performance and core business success—a dynamic the market consistently rewards across exchange tokens.

Relative Valuation Analysis: Exchange Token Divergence

And this leads to the perfect segue into talking about how Bybit and Mantle are positioned versus the other CEXes. Exchange tokens are experiencing sector-wide appreciation, yet significant valuation disparities have emerged. Comparative analysis across major exchange tokens reveals MNT trading at a substantial discount to peers despite comparable underlying business metrics:

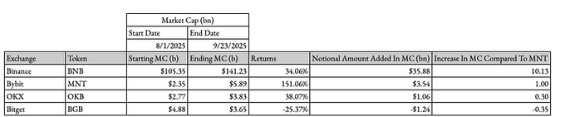

Since August 1 2025, exchange tokens have posted strong gains:

- ◆BNB: +$35B market cap increase

- ◆OKB: Significant appreciation following supply reduction

- ◆BGB: Strong performance amid burn programs

- ◆MNT: +$3.5B market cap increase (9x less than BNB)

There is a volume-to-valuation disconnect. Since August 1st, BNB added 10x more than MNT’s $3.5 billion increase during the same period. Yet here’s the kicker: Bybit consistently does about one-third of Binance’s trading volume across spot and derivatives.

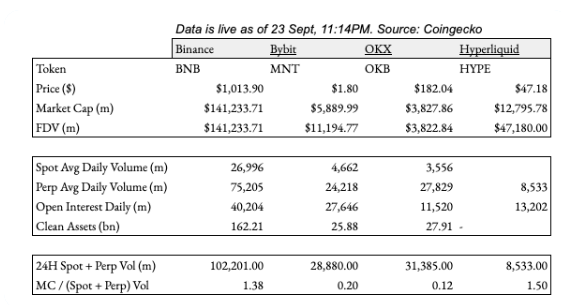

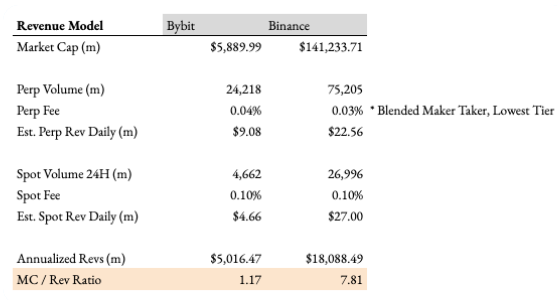

The trading volume analysis reveals a fundamental mispricing. Looking at market-cap-to-volume ratios, this is even clearer:

- ◆MNT: 0.12x

- ◆BNB: 1.15x

- ◆HYPE: 1.05x

MNT trades at a ~10x discount to BNB on this metric, despite representing exposure to comparable trading infrastructure and revenue generation. Lastly, according to the assumed revenue models, MNT trades at less than 1x MC/Rev, while BNB trades at ~7.26x. In any case, MNT has room to grow.

Structural Differentiation from OKX

While OKX appears similarly positioned by volume metrics, critical structural differences limit OKB's utility integration. OKX does not incorporate OKB holdings into trading fee calculations, eliminating a key demand driver that Bybit has committed to implementing for MNT.

Source: OKX Fees

On top of that, OKB's value proposition on its website centers on launchpad access and staking rewards rather than core exchange utility integration. This limits structural demand drivers and suggests OKX's recent burn initiatives may be reactive rather than strategic.

The Information Gap

There's also an underappreciated geographic component to this opportunity. Eastern-focused exchanges face systematic undervaluation in Western markets due to information flow disparities. Binance achieved global recognition, but Bybit remains more regionally focused despite comparable operational scale.

This creates exactly the kind of information asymmetry that generates alpha - when comparable assets trade at different valuations because one market understands the story better than another. The opportunity exists in that gap between Eastern operational reality and Western market perception.

Execution & Strategic Positioning

Overall, when compared to CEXes other than Binance, Bybyt’s approach seems to have a much higher level of management execution and strategic vision. With CEO-level commitment behind the initiative, MNT is now a core priority and isn’t just a side project. It is at the beginning of its utility integration journey, with each integration milestone representing a catalyst that the market hasn't fully priced in yet.

Timing and Risk Assessment

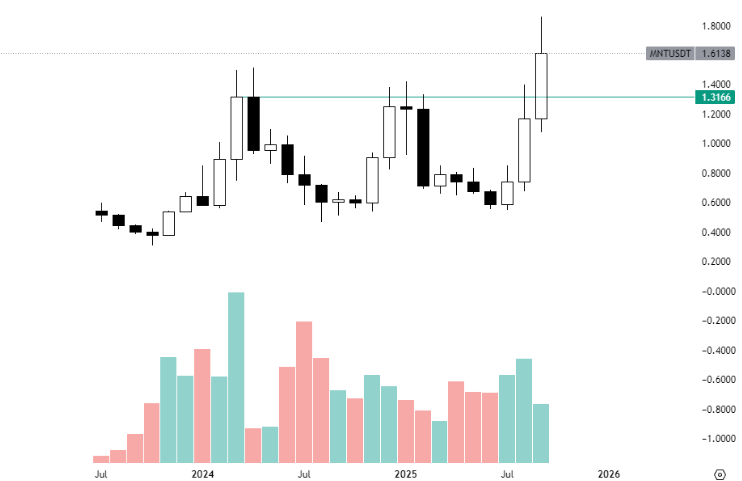

Let's address the elephant in the room: MNT has been a notorious trade in Asian crypto circles for four years. The chart tells the story - multiple failed breakout attempts based on speculation about Bybit integration that never materialized.

Why This Time Is Different

Previous MNT rallies were built on hope rather than substance. For four years, MNT existed as a standalone L2 token with Bybit ownership but zero operational synergies. The timeline reveals the progression:

- ◆August 2021: Launched as BITDAO (investment DAO token)

- ◆May 2023: Converted to MNT, pivoted to L2 focus

- ◆July 2025: First real Bybit integration announcements

- ◆August 2025: Bybit executives joined Mantle's advisory board

The belief is that the current breakout reflects actual integration progress rather than speculative positioning. With operational convergence between Bybit’s exchange infrastructure and Mantle’s utility function, this time does signify a trend shift in Mantle’s lifecycle.

Risk #1: Execution Failure

The primary risk remains Bybit under-delivering on integration promises. If promised fee discounts, leverage features, or OTC portal rollouts are delayed or implemented poorly, the utility narrative collapses entirely.

Mitigation: Recent signals suggest serious commitment. In a BidClub interview, Emily (Head of Spot Business at Bybit and Key Advisor at Mantle) described the timeline as "ASAP given CEO Ben's urgency." More importantly, institutional client communications from September 10th confirm Bybit has been delivering on outlined promises to date.

Source: @Cptn3mox on X

Risk #2: Competitive Displacement

BNB maintains massive advantages through proven utility and institutional adoption. Accelerated innovation from Binance or other exchanges could overshadow MNT despite strong fundamentals.

Mitigation: Multiple exchange tokens can coexist successfully, similar to L1 ecosystems or derivatives platforms. Each exchange serves distinct market segments—Binance focuses on retail and global reach, while Bybit specializes in derivatives and institutional trading. MNT can establish dominance in the derivatives-focused, Asia-centric segment without direct competition with BNB's retail-oriented utility.

Risk #3: Sector Timing

Entry may be occurring late in the exchange token cycle. BNB, OKB, and peers have already posted significant gains in 2024-2025, potentially limiting upside for late entrants.

Mitigation: Exchange tokens remain early-stage relative to traditional finance penetration. More critically, MNT represents a 0-to-1 utility integration story while peers have matured. Even in bear markets, exchanges with strong utility tokens often gain market share as cost savings become more valuable when margins compress.

Risk #4: Geographic Constraints

Bybit's exclusion from major markets (US, UK) caps total addressable market compared to regionally-focused competitors like Coinbase.

Mitigation: This constraint may be diminishing rapidly. Acting CFTC Chairman Caroline Pham recently announced plans to allow US citizens to trade on offshore exchanges under CFTC regulations, specifically mentioning Binance, Bybit, and OKX. This regulatory shift could unlock significant growth potential without requiring separate US entity establishment.

Conclusion

MNT appears positioned at the beginning of its utility integration cycle rather than the end. The combination of concrete operational progress, structural demand drivers, and potential regulatory tailwinds creates an asymmetric opportunity as the market transitions from speculation to substance.

The four-year false starts actually strengthen the current thesis—previous failures were based on hope, while current momentum reflects operational reality. When speculation finally aligns with execution, the repricing can be dramatic.

IMPORTANT NOTICE: This document is intended for informational purposes only. The views expressed in this document are not, and should not be construed as, investment advice or recommendations. Recipients of this document should do their own due diligence, taking into account their specific financial circumstances, investment objectives and risk tolerance (which are not considered in this document) before investing. This document is not an offer, nor the solicitation of an offer, to buy or sell any of the assets mentioned herein.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

0

0