GEODNET December Update: Scaling Revenue, Compressed Valuation

Introduction

Geodnet is already widely used in industries where very high positioning accuracy is essential, including agriculture and construction. In farming, tractors rely on centimeter-level GPS for precise steering, planting, fertilizing, and harvesting, while spraying drones use it to apply chemicals accurately, avoid overlaps, and reduce waste. In construction, the same level of precision is used by automated machinery and drones for accurate machine guidance, site layout, and earthworks.

Traditional positioning systems usually rely on closed, proprietary hardware costing around $8,000 per unit. If a user’s location is not covered by an existing network or if no subscription is purchased, the customer must build and maintain their own infrastructure. The largest traditional competitor offers the same RTK correction service for approximately $100 per month for a single location, while Geodnet provides the same service for around $40 per month.

By comparison, Geodnet operates a global network of over 21,100 reference stations, while its largest traditional competitor runs roughly 5,300 stations. That competitor’s parent company trades at a valuation of approximately $30.6B, even though precise positioning services represent only 20-30% of its total business. If that company were focused exclusively on precise positioning, this would imply a standalone company valuation of approximately $6-9B. Notably, this company trades at a P/E multiple roughly 2x higher than Geodnet’s.

Geodnet delivers the same centimeter-level accuracy with hardware costing around $695, while also providing access to a large, shared global network. This makes Geodnet a far cheaper, more scalable, and more practical solution for modern agriculture, construction, and drone-based operations.

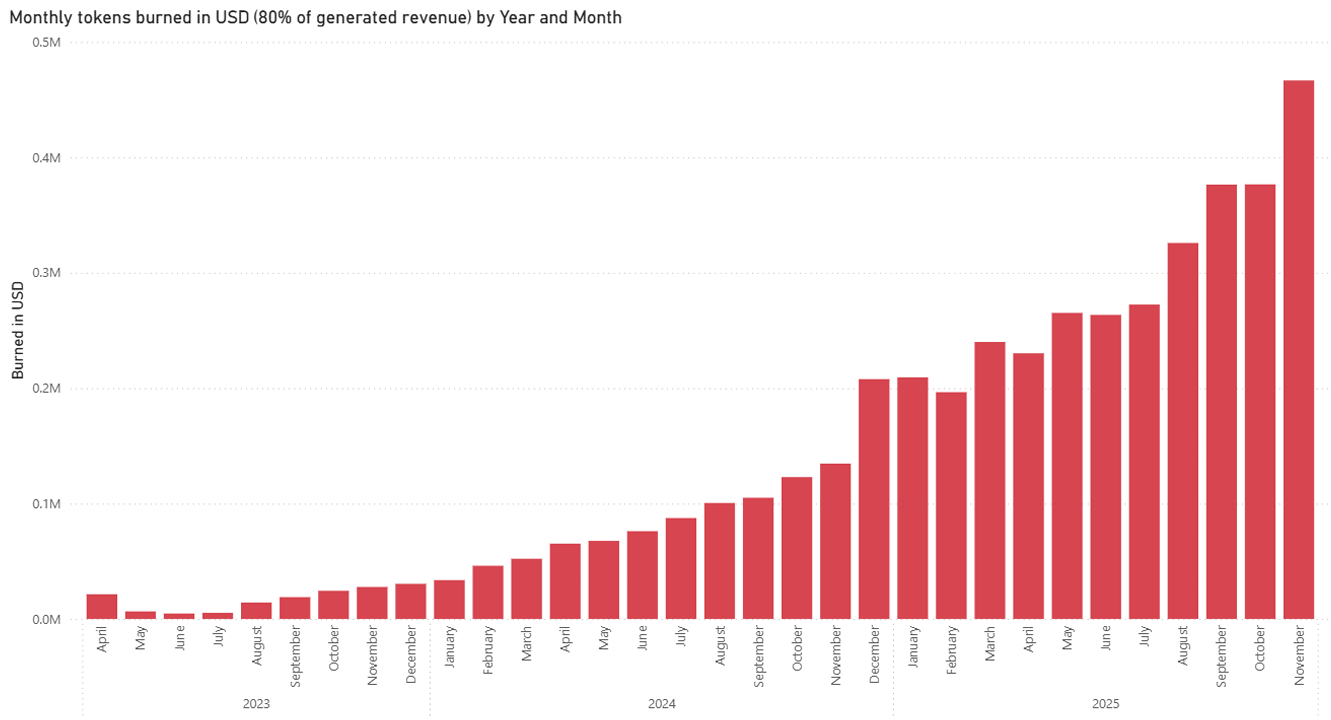

Monthly burn in USD

These figures represent tokens burned in USD, where 80% of total generated revenue is burned and the remaining 20% is allocated to the company. (In the chart, the figures are shown after deducting 20% from revenue).

Revenue has grown strongly and consistently over time, with monthly tokens burned increasing from about $21k in April 2023 to roughly $467k in November 2025, representing more than a 20x increase. On average, this implies around 10% compound monthly growth, which is very strong for a revenue-linked metric.

Over the past year, growth remained strong, with monthly tokens burned increasing by approximately +246% YoY from November 2024 to November 2025. During this period, revenue continued to scale on a MoM basis, with recurring MoM increases typically in the +5-15% range, reflecting sustained demand and improving monetization.

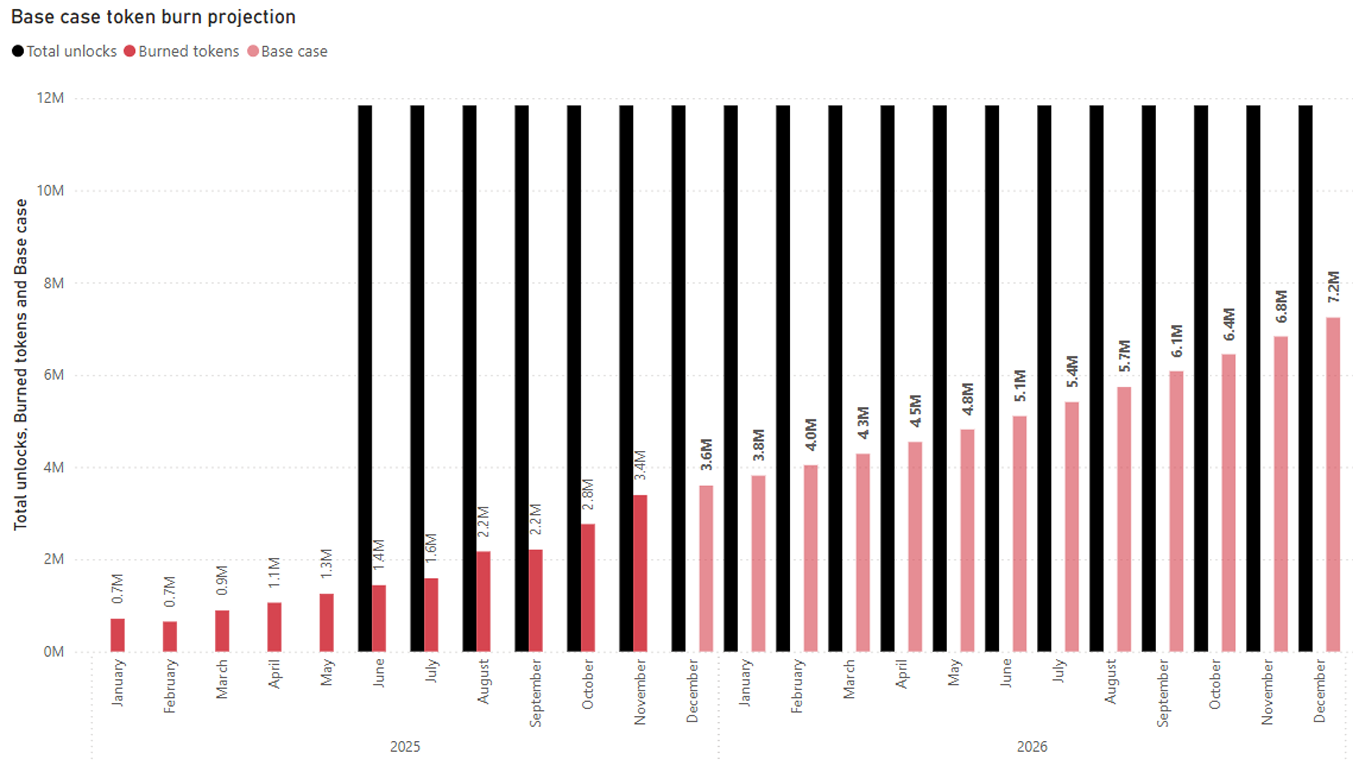

Token burns and vesting schedule

The chart shows planned token unlocks (black), tokens burned (red), and forecasted future token burns (transparent orange). Token unlocks also occurred in previous years, but they were concentrated in a few large events rather than distributed over time. Starting in June this year, unlocks became stable and recurring and are expected to continue for several years. It is important that the burn rate scales toward the level of unlocked tokens to avoid excessive sell pressure. Full token unlock schedule.

Future monthly burned tokens are projected using a constant 6% MoM growth rate, derived by normalizing the historical ~18% average monthly burn growth with an approximately 65% risk haircut. This rate reflects steady net subscription growth and assumes token burn scales proportionally with platform usage, independent of crypto market performance.

Historically, burn growth exceeded the forward-looking assumption and included periods of strong double digit MoM expansion. The model deliberately applies a more conservative growth rate than historical peaks to mitigate the risk of overstating future performance.

Token unlocks are currently distributed as follows: Team 42.64%, Investors 32.70%, Mining rewards 14.84%, Ecosystem 7.38%, and Vendors 2.45%. The team has not sold any of its tokens to date, as confirmed by the team wallet, and most investor wallets also appear inactive and well controlled. As a result, the only consistent sources of sell pressure are vendors receiving token rewards for selling Geodnet devices and miners realizing mining rewards.

Geodnet compared to other crypto DePIN projects

Geodnet does not face direct competitors within the crypto sector. However, it competes indirectly with other decentralized networks that require users to deploy physical devices in specific locations. As a result, it is critical to understand which device a user is likely to choose when deciding to contribute to a network (compared with Helium and Hivemapper):

Comparison of device costs, days to breakeven, and estimated daily returns across each project:

The figures shown assume ideal conditions, meaning maximum rewards are only achievable when optimal setup requirements are met. In Geodnet’s case, these conditions are relatively easy to satisfy: a miner simply needs to be deployed in a hex without an existing station, which is still widely achievable across the network.

By contrast, Helium’s network is heavily oversaturated, making it nearly impossible for new miners to achieve optimal rewards. Reaching peak performance often requires hardware modifications, additional antennas, and strong technical expertise in RF networking. Hivemapper faces a different constraint: to earn maximum rewards, operators must drive approximately 124 miles (200 km) per day on roads that are not yet mapped, which significantly limits accessibility for new participants.

Low and declining rewards discourage new miner deployments over time. Maintaining a healthy balance between miner count and individual rewards is critical for long-term network growth. Geodnet addressed this issue before launch through its hex-based incentive and reward structure, while oversaturation has become a structural problem that Helium and Hivemapper can no longer realistically fix.

Geodnet has also released a miner priced at $1,095 that mines not only GEOD, but also Wingbits points (which are expected to convert into tokens). Wingbits is a DePIN project focused on aviation, backed by $9.1M in funding from Tribe Capital, Spartan Group, Borderless Capital, and others. This is another innovation that enables users to earn rewards from multiple DePIN networks using a single device, while maximizing rewards without requiring any technical expertise.

Emissions and halving dynamics

Geodnet implements an annual halving, meaning miner rewards are reduced by half every summer. On the positive side, this is healthy for token economics, as Geodnet mining emissions represent pure sell pressure. Currently, mining emissions account for approximately 4.07M GEOD per month, while the current burn rate is around 3.4M GEOD per month, significantly offsetting the associated sell pressure.

The primary risk of this model is that if the token price does not increase after a halving, miner rewards in dollar terms could decline materially, potentially reducing miner participation. However, following a direct discussion with the founder, it was confirmed that if this scenario emerges, Geodnet plans to introduce staking, with staking rewards paid in stablecoins.

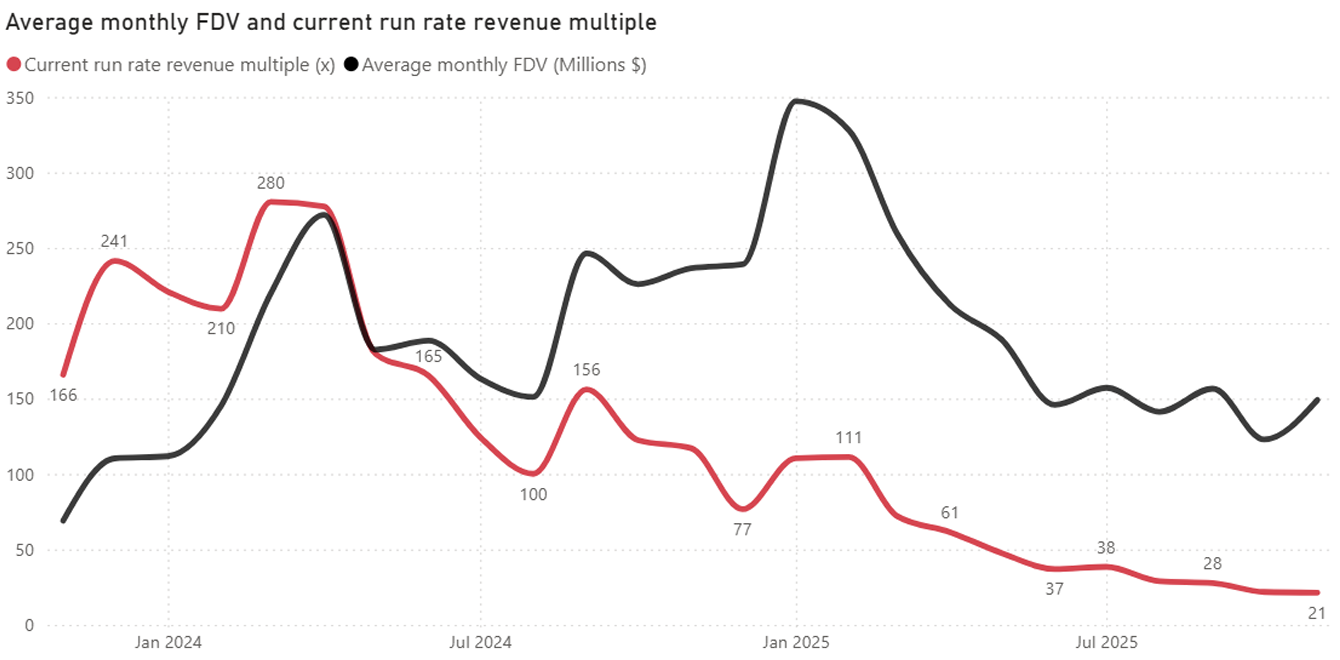

Current valuation

The chart indicates a significant compression in the run-rate revenue multiple, which has declined sharply over the period and now sits near cycle lows. This means the project is currently being valued at a much lower multiple relative to its revenue generation than at any prior point in the period shown. In practical terms, revenue growth has materially outpaced valuation, suggesting the market has not yet fully reflected the underlying business performance. At current levels, the data points toward the asset being priced conservatively relative to its fundamentals, which can reasonably be interpreted as a sign of undervaluation rather than weakening demand or deteriorating operations.

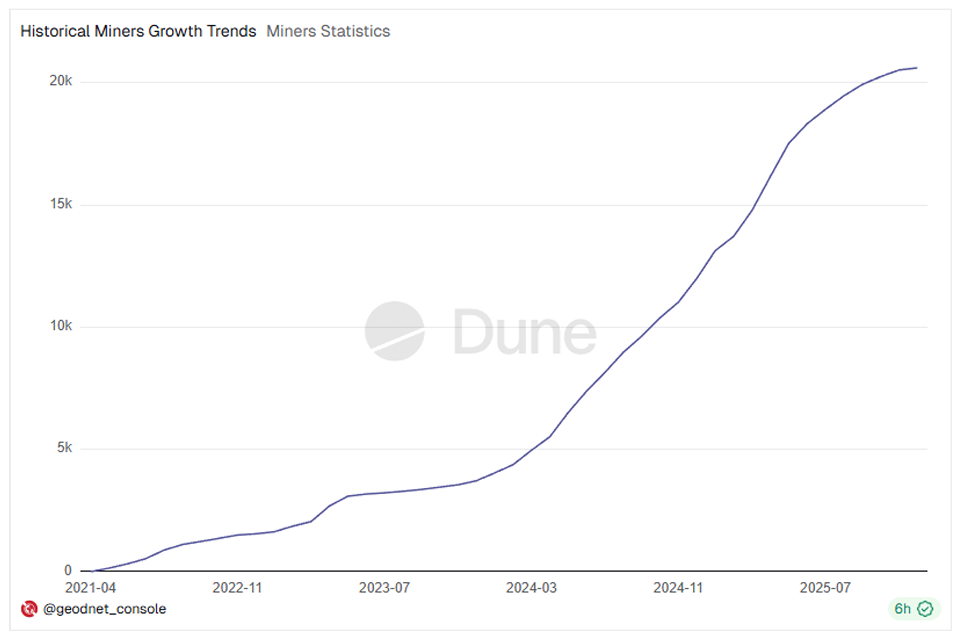

Growth in deployed miner devices

The data shows continued MoM growth from November 2024 through November 2025. Growth remains positive throughout the period, initially running at higher single-digit MoM rates before gradually moderating to approximately 1-3% MoM toward late 2025. This deceleration reflects controlled and intentional scaling rather than a loss of momentum. Miner density remains unsaturated, rewards are not diluted across an excessive number of participants, and incremental deployments are increasingly directed toward geographies where coverage demand is highest. Overall, the MoM trend stays consistently upward with no periods of contraction, indicating a transition toward stable, demand-driven network expansion.

It is important to understand the ownership structure of miners within this ecosystem.. From the early stages of the project, there was strong interest from real businesses, not just individual operators. Because the network was initially underdeveloped, especially in regions such as South America, many companies began deploying their own Geodnet GNSS stations to use the service in their area, while also earning mining rewards and purchasing subscriptions. This was economically rational, as Geodnet’s solution was significantly cheaper than traditional positioning providers. As a result, there are now multiple businesses and operators that own hundreds of miners, using the network operationally while earning rewards from the infrastructure they operate.

What’s next?

GEO-Swarm is a drone-based home and property security product that GeodNet is preparing to launch. The concept is simple: instead of fixed cameras, the system uses one or more small autonomous drones that patrol a predefined area around a house, construction site, or facility. These drones rely on GeodNet’s positioning data to know their exact location down to centimeters, so they can follow the same flight paths every time, return to precise docking points, and operate safely around buildings, fences, and other obstacles.

For Geodnet, the benefit is practical and direct. Every drone needs constant high-accuracy location data, which it gets from the GeodNet network. That means the drones become paying users of GeodNet’s RTK service, increasing real demand for the network’s data.

In my view, the primary growth trigger is not GEO-Swarm, but the U.S. government’s accelerating shift toward drones and autonomous systems. Over the past several years, U.S. federal spending on unmanned platforms has grown at a high-single to low-double-digit annual rate, while spending on manned systems has remained flat. This reflects a clear reallocation of procurement budgets toward autonomy, making high precision positioning a structural requirement rather than an optional capability.

Conclusion

This is a strong opportunity to gain an edge by understanding the project’s mechanics while gaining exposure to robotics at an attractive valuation compared to traditional companies. It is one of the clearest examples of crypto rails being used in traditional businesses, and project metrics are largely unaffected by broader crypto market conditions. The category is fast growing and supported by strong backing and a team with deep domain expertise, and lessons learned from past DePIN failures have resulted in one of the strongest DePIN infrastructures in its category.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

0

0