$SHFL: How One of Crypto’s Strongest Cashflow Stories Could Break Into the Top 100

Since publishing my original Shuffle report for Delphi on July 7th, the project has delivered solid progress across the board. Beyond $SHFL’s price appreciation, we’ve seen clear growth in NGR (net gaming revenue), steady user engagement, and lottery dynamics that continue to validate the core thesis.

In this update, I’ll break down why I remain bullish on $SHFLas a cornerstone of crypto’s emerging “revenue meta,” highlight key catalysts on the horizon, and outline a few steps the team could take to accelerate a rerating.

With the right adjustments and as the market begins to recognize SHFL’s underlying business strength, I see a credible path for Shuffle to break into the top 100 coins by market cap (from its current rank of #455).

With that backdrop, we can turn to what has happened since July 7, both in $SHFL’s market performance and in the fundamentals of its underlying business.

Growth on Both Fronts: $SHFL’s Price, Revenue, and Lottery Dynamics

Since July 7th, $SHFLhas climbed roughly 80%, moving from $0.21 to around $0.38 today. That translates to a circulating market cap increase from just under $70 million to around $125 million, with FDV expanding to ~$360 million.

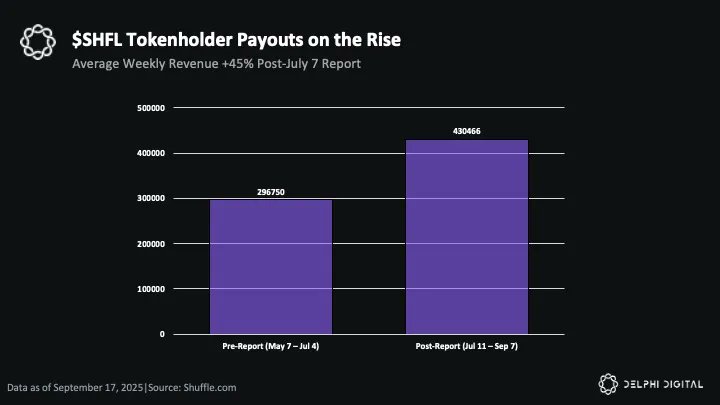

Over the same stretch, Shuffle’s business fundamentals have continued to strengthen. In the 60 days prior to my July 7th report (lotteries from May 7 to July 4), the lottery was averaging ~$297k in weekly NGR added for stakers.

In the 60 days after (July 11 to September 7), that figure climbed to ~$430k, a 45% increase. On a business-wide basis, this equates to total weekly NGR rising from about $1.98m to $2.87m. While it is still early to judge the long-term sustainability of this growth, the trajectory is undeniably impressive.

https://x.com/shufflecom/status/1948651722387456302

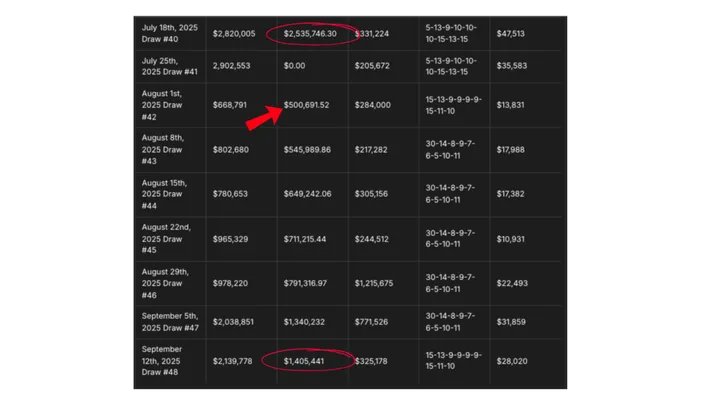

Additionally, during this same stretch a $SHFLstaker won the lottery’s main jackpot for the first time, taking home more than $2.5 million. It was a landmark event and a strong complement to the usual pro-rata yield distribution.

Following the payout, the team injected another $500k into the pool, and after six weeks of contributions the jackpot has already climbed back to roughly $1.4m. It continues to function as both a compelling marketing draw and a built-in call option that keeps users engaged and looking ahead to the next big prize.

Relative Value Check: Why $SHFL’s Cashflows Outsize Its Market Cap

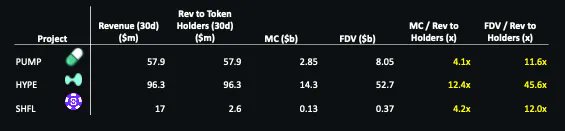

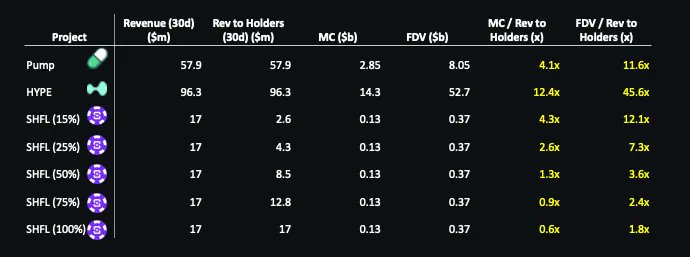

When stacked against the blue-chips of the revenue meta, Hyperliquid ($HYPE) and Pumpfun ($PUMP),$SHFLcomes out looking relatively fairly valued, with the verdict hinging on how you rate its revenue delivery model.

For HYPE and PUMP, nearly all revenue flows back through buybacks (~99% of fees for HYPE and effectively 100% of revenue for PUMP, though in Pump’s case this level of buybacks is a recent development and it remains to be seen if they can sustain it). Shuffle trades at ~4.2x MC/rev-to-holders compared to Pump’s 4.1x and HYPE’s 12.4x, with similar ratios across FDV multiples.

The difference is that PUMP and HYPE are already priced at their theoretical maximum of 100% value capture. SHFL, by contrast, distributes just 15% of revenue today, leaving enormous upside potential that isn’t yet priced in. Management has previously signaled openness to increasing tokenholder capture, and unlike most protocols, that shift could be enacted overnight. In other words, SHFL carries embedded option value: the chance for tokenholder economics to materially improve with a single policy change.

And critically, the form of distribution matters. While buybacks can support price and align incentives, USDC dividends are more tangible. Dollars recycled into the chart don’t always guarantee a positive impact on token price, and even when they do, holders don’t necessarily realize those gains. Fresh USDC in your wallet, on the other hand, is immediately real: it can be spent, reinvested, or wagered however you see fit.

From this perspective, one could argue that Shuffle’s “revenue to tokenholders” is actually more valuable, though this point is open to debate.

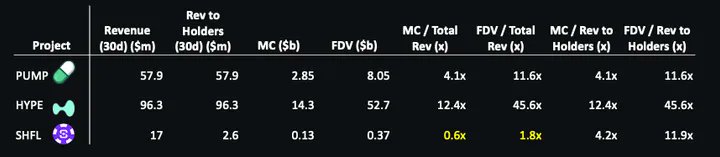

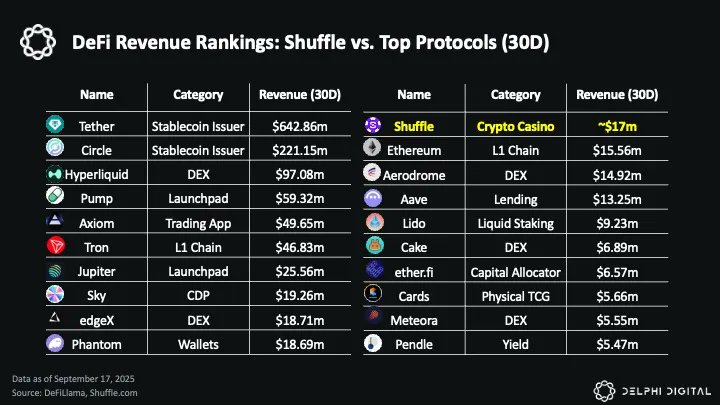

Regardless, Shuffle generated over $17 million in revenue last month on a market cap that is just a fraction of Pump’s $2.8b and Hyperliquid’s $14b. On a total revenue basis, that equates to only ~0.6x MC/Rev and ~1.8x FDV/Rev, compared to Pump at 4.1x and 11.6x and HYPE at 12.4x and 45.6x.

Proportionally, SHFL is producing an outsized amount of revenue relative to its size.

And it’s not just relative to Pumpfun or Hyperliquid. Across DeFi as a whole, Shuffle’s ~$17m in trailing 30-day revenue would rank it #11 among all protocols. To put that in context, that’s more than Ethereum itself generated over the same period (~$15.6m) and just shy of Phantom’s ~$18.7m.

This isn’t a one-off spike either, Shuffle has consistently delivered revenues at this scale, a trend clearly reflected in the weekly lottery history of NGR added.Paired with its comparatively small market cap, this level of output underscores the strength of its business model and the magnitude of rerating potential if a larger share of revenue is directed to tokenholders.

Beyond the USDC yield, Shuffle also returns value through buybacks and burns, allocating 30% of all NGR generated from users betting their $SHFL. Over the past four weeks, this has averaged about $45.5k per week (~$181.6k total), all executed transparentlyon-chain.

While this figure isn’t yet large enough to shift the relative valuation picture, it does highlight the optionality management has in shaping tokenholder value capture. Striking the right balance between USDC distributions and buybacks could become a powerful lever for long-term appreciation in $SHFL, and it’s an area where I see clear room for improvement if the team leans into it…

From Equity Overhang to Rerating: How $SHFLCan Break Into the Top 100

There’s no doubt Shuffle is an incredible business, a true cash cow, but it still has equity holders and investors receiving unlocks. This is the biggest structural overhang. Should Shuffle collapse its equity and push cash flows fully into the token, it could position itself as the “Hyperliquid of gambling”, or perhaps with an even broader appeal, as owning a share of one of the world’s largest online casinos.

One way to feasibly achieve this, as I see it, would be granting equity holders treasury tokens in exchange for their equity stakes. This creates a mutually beneficial setup where both sides win:

- ◆Tokenholders see cash rewards jump 6x overnight (from 15% to 100%), triggering a sharp rerating.

- ◆Equity holders would likely end up with treasury token allocations worth more than their original equity, while also gaining liquidity.

In practical terms, collapsing equity and shifting to a PUMP/HYPE-style model would be transformative.

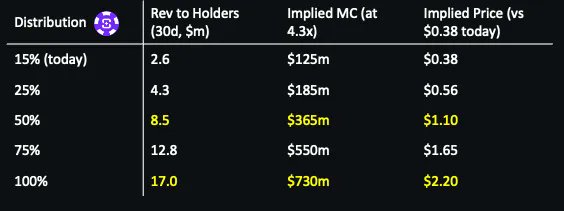

Today, as previously mentioned,$SHFLdistributes just 15% of revenue to tokenholders. If that were increased to 25%, 50%, 75%, or even 100%, the valuation picture changes dramatically:

At the current 15% distribution, SHFL trades at ~4.3x MC/Rev-to-holders and ~12.1x FDV/Rev-to-holders, which screens roughly in line with Pump and materially cheaper than Hyperliquid. But the bigger takeaway is what happens if Shuffle ever reallocates a larger share of NGR toward tokenholders.

Even a modest step up to 25% or 50% distribution would drop SHFL’s multiples into the 2.6x–1.3x range on circulating market cap. At 100% distribution, SHFL would trade at just 0.6x MC/Rev-to-holders and 1.8x on an FDV basis, making it one of the cheapest assets in all of crypto and a clear standard-bearer for the “revenue meta.”

At that level, the token would effectively be yielding north of 150% annually at today’s market cap, a figure almost impossible for investors to ignore. It would not only put Shuffle at the center of the “revenue meta” narrative, but could also revive attention toward the largely unloved online casino sector within crypto.

Another way to frame the upside is by holding SHFL’s current ~4.3x MC/Rev-to-holders and ~12.1x FDV/Rev-to-holders multiples constant. On that basis, a 50% distribution would imply a ~$365m market cap and ~$1.03b FDV, just outside the current top 100 threshold, and a token price of ~$1.10, nearly a 3x from today’s ~$125m market cap and $0.38 price.

At 75% distribution, SHFL would rerate to a ~$550m market cap and ~$1.55b FDV, or ~$1.65 per token (a ~4x from current levels). And at 100% distribution, SHFL would climb to ~$731m market cap and ~$2.06b FDV, equating to ~$2.20 per token, nearly a 6x from where it trades today.

With the current cutoff for the top 100 coins sitting around a ~$1.3b market cap, it’s clear that reallocating more of Shuffle’s revenue to tokenholders would be enough to push $SHFLinto that bracket even without multiple expansion. The path is already embedded in the business, it simply comes down to how aggressively management chooses to return cash flows to tokenholders.

Importantly, Shuffle’s revenues are also not as tightly correlated with market volatility as DEXs, launchpads, or other crypto-native businesses. That resilience makes it a uniquely compelling asset for bear market positioning, where steady, non-cyclical cash flow can become even more valuable.

While such a structural change may take time, with gradual increases above the current 15% threshold more likely than an overnight shift, it is in my view the single most important step for Shuffle to truly rerate and establish itself as a dominant crypto asset.

Beyond Equity Collapse: Secondary Drivers for SHFL’s Rerating

While collapsing equity remains the single largest unlock for SHFL, there are a number of secondary drivers that could still support a meaningful rerating in the near to medium term:

Onchain lottery rollout + permissionless staking

- ◆Building out Shuffle’s vision for the world’s largest permissionless lottery could be a massive driver of future NGR growth and token flows.

- ◆Even moving the current setup into a more self-custodial format would unlock participation from firms and institutions restricted from depositing directly into casinos or LPs, a major bottleneck today.

Increased visibility & transparency

- ◆A public buyback dashboard (like HyperDash or Pump’s) would meaningfully improve visibility in the “revenue meta,” boosting awareness and reflexivity as results get widely shared.

- ◆Similarly, a listing on DeFiLlama would put SHFL firmly on the radar of investors tracking protocol revenues, helping cement it as a potential “blue-chip” in the sector.

Exchange listings + liquidity

- ◆SHFL is still absent from major exchanges. Broader tier-1 listings would open the door for less crypto-native capital, improving price discovery and liquidity depth.

- ◆On the decentralized side, the trend of Hyperliquid spot listings, as seen with PUMP and FARTCOIN, has shown how quickly a gambling coin, or any strong fundamental token with real demand, can rerate once key access barriers are removed. That said, CEX listings remain a valuable on/off-ramp, particularly given Shuffle’s business model

Chain migration (Sol -> ETH)

- ◆A potential migration (from ETH to Solana) could align SHFL with its user base, many of whom are less crypto-native gamblers already transacting on Solana.

- ◆While not the most immediate bottleneck, collaboration with a Layer-1 ecosystem with broad distribution (e.g., Solana) could establish SHFL’s onchain home and create a symbiotic growth channel.

Lend/borrow markets

- ◆While lower priority, introducing lending/borrowing functionality for SHFL could create new use cases and incremental liquidity. Any such markets would likely need very conservative LTVs given the token’s liquidity profile and potential volatility.

- ◆Even so, some holders may be willing to forfeit their lottery dividend yield in order to unlock liquidity and deploy capital into other onchain opportunities without selling their SHFL outright.

Team visibility & thought leadership

- ◆More appearances on podcasts and industry discussions, similar to Pump’s recent efforts and Jeff from Hyperliquid’s occasional outreach, would reinforce credibility.

- ◆Shuffle’s founders are fully doxxed, crypto-native, and relatively young, a rarity in both the casino industry and crypto. They have compelling stories to tell, and greater transparency or public-facing updates could help more people rally around the team and get excited about SHFL.

Geographic expansion (Shuffle(.)US)

- ◆The upcoming U.S. rollout could prove a major growth driver, bringing Shuffle into the single largest regulated betting market.

- ◆While this has likely pulled focus from other initiatives in the near term, once live it could be a serious lever for NGR expansion.

Balance sheet strength

- ◆Finally, while not publicly disclosed, it’s likely the Shuffle team has built a substantial balance sheet alongside its bankroll.

- ◆This capital can be deployed strategically, whether for growth initiatives, marketing, or to accelerate some of the catalysts mentioned above. While the team is understandably cautious about disclosing exact figures to avoid giving competitors an edge, their balance sheet does appear large enough to sustain buybacks and lottery injections (dividends) while still leaving room to fund growth initiatives, depending on how heavily they choose to prioritize tokenholders.

- ◆

Conclusion: Embedded Option Value That the Market Hasn’t Priced In

Shuffle is already operating at a scale that most protocols, and businesses more broadly, can only dream of, consistently generating ~$17m a month in revenue, more than Ethereum itself over the same stretch, while trading at just a ~$330m FDV. Proportionally, it is one of the most cash-generative assets in all of crypto, yet its tokenholders capture only 15% of that flow today.

That’s the crux of the opportunity. Unlike Pumpfun and Hyperliquid, already priced at their theoretical maximum of 100% value capture, SHFL still carries embedded option value. Management has signaled openness to increasing tokenholder distributions, and such a change could be enacted overnight. A move from 15% to full revenue-to-tokenholder alignment would unlock a 6x jump in cash flows, push effective yields north of 150% (though dependent on how the token rerates), and in my view, all but guarantee an eventual move into the top 100.

Even short of that structural shift, multiple catalysts: from an onchain lottery rollout and permissionless staking, exchange listings, chain partnerships, and the U.S. launch, can keep driving growth and market recognition. A robust balance sheet and healthy bankroll give Shuffle the resources needed to double down on growth and strategic initiatives.

Put simply: the value is already there, which is rare in crypto. It just needs to be unlocked. Whether through incremental adjustments or a full equity collapse, I see SHFL as one of the clearest asymmetric opportunities in the entire market today.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

9

0