Euler ($EUL): A Mispriced DeFi Blue-Chip with Explosive TVL, New Revenue Lines, and Institutional Tailwinds

Summary

- ◆TVL growth outpaces token appreciation — TVL grew 200x ($10M → $2.3B) in last 9 months while token market cap only grew 4x ($50M → $200M)

- ◆Attractive financial metrics like 52% borrow efficiency (ranking highest among peers) and trades at a 14x FDV/Fees ratio

- ◆EulerSwap launch creates new revenue streams beyond traditional lending and early traction ($700M cumulative volume in 2 weeks) shows strong PMF

- ◆Institutional adoption with BlackRock’s BUIDL fund and Unichain narrative present strong secondary catalysts

- ◆Similar setup to PENDLE and SYRUP before their CEX listings: strong fundamentals, high circulating supply, and low FDV (~$290M)

Resilient company history

Euler Finance (“Euler”) has a resilient history marked by both challenges and achievements.

Founded in 2020, the company raised over $40M from prestigious investors including Paradigm, Haun Ventures and Coinbase Ventures. After launching its v1 mainnet in December 2021 and eclipsing $600M TVL in under a year, Euler faced a severe setback in March 2023 when a hack drained $200M in protocol liquidity. Demonstrating remarkable resilience, the team recovered all funds plus an additional $40M by April 2023.

Instead of rushing back to market, Euler shut down v1 and spent the bear market rebuilding, investing millions in 45 security audits conducted by 13 different firms.

The company relaunched Euler v2 in stealth in Q4 2024, gradually rebuilding TVL to $100M by January 2025, and has since experienced explosive growth to $1.1B TVL as of June 2025 when they also launched EulerSwap.

Euler is a multi-pronged product within DeFi’s largest verticals

1. Lending — Euler v2

Euler Finance (Euler v2) is a modular DeFi lending protocol on Ethereum, enabling permissionless lending and borrowing of any ERC-20 asset, including long-tail tokens. Through Euler, any asset can become collateral for a lending market.

Its distinct features include:

- ◆Permissionless Lending & Borrowing: Users can create lending markets for any ERC-20 token with a WETH trading pair on Uniswap v3, supporting niche/volatile assets without requiring governance approval.

- ◆Modular Architecture: Lets protocols create and manage lending markets tailored to their needs — Euler Vault Kit (EVK) enables custom lending vaults in ERC-4626 standard and the Ethereum Vault Connector (EVC) allows cross-vault collateralisation for composability.

- ◆Risk Management: Euler v2 has sophisticated risk controls.

- ◆Asset Tiers: Assets are categorised into tiers such as Isolation (high-risk, borrow-only), Cross (borrowable, non-collateral), and Collateral (low-risk, collateral-eligible) to mitigate volatility risks.

- ◆Sub-Accounts: Users can create up to 256 sub-accounts per Ethereum address to isolate positions, reducing systemic risk.

- ◆Soft Liquidations: Liquidations use Dutch auctions with dynamic discounts (up to 20%), ensuring cost-effective outcomes compared to fixed-rate models.

- ◆Protected Collateral: Lenders can deposit assets as “protected collateral,” which cannot be lent out, offering risk-free exposure with instant withdrawal.

- ◆Reactive Interest Rates: Dynamically adjust interest rates based on vault utilisation, compounded per second, ensuring capital efficiency.

- ◆Fee Flow & Rewards: MEV-resistant Fee Flow auctions, distributes protocol fees to EUL holders (more on this below).

- ◆Oracles: Uses Uniswap v3 TWAP as its primary pricing oracle, with support from Chainlink feeds, and has an Oracle Rating system to evaluate oracle reliability based on manipulation resistance.

- ◆Security: Protocol-owned liquidity reserves provide a backstop against liquidity crises.

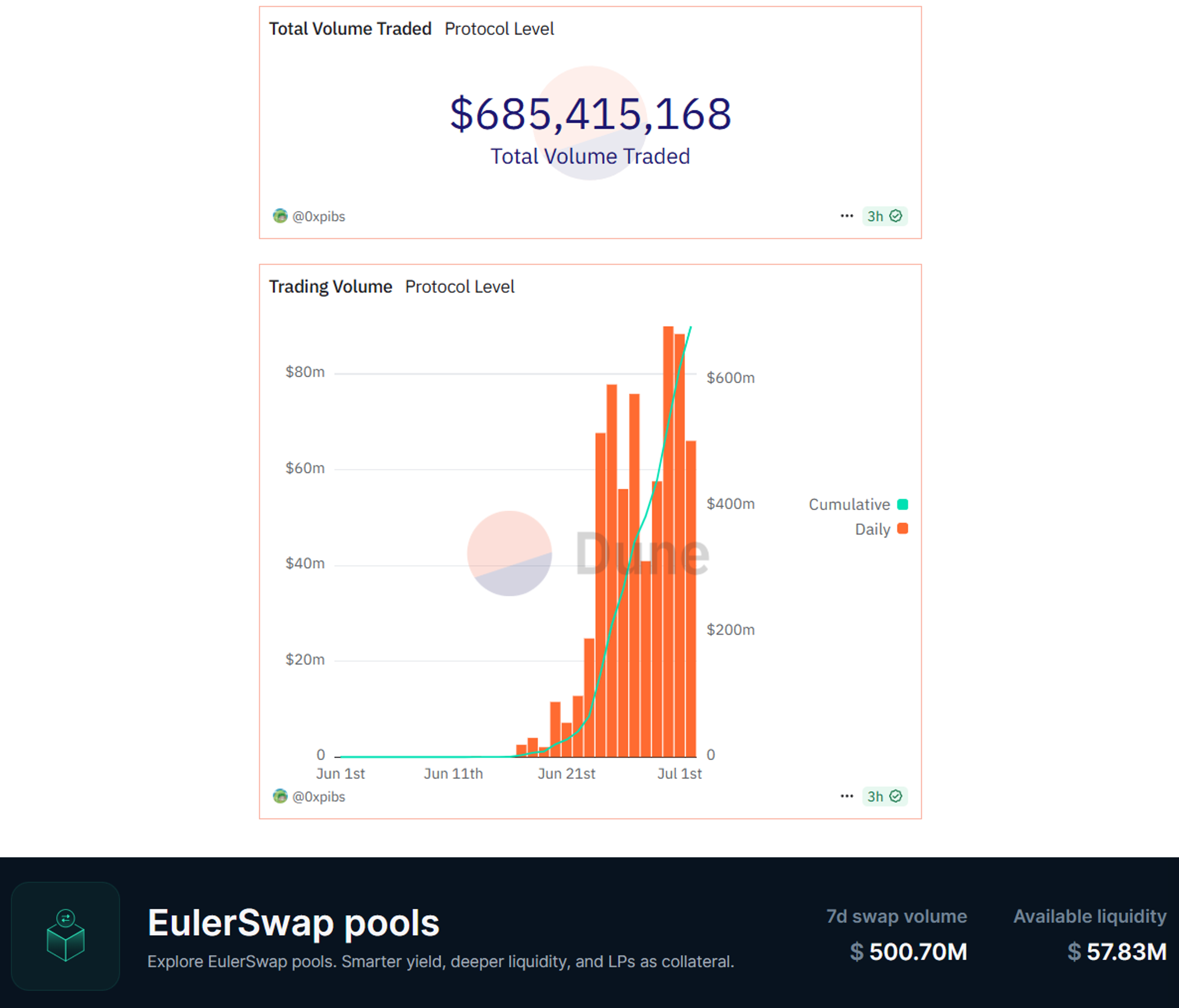

2. DEX — EulerSwap

EulerSwap is a DEX within Euler that just launched in June 2025 (2 weeks ago at the time of writing).

This is a new innovation of a DEX within a money market, that turns idle lending liquidity into productive capital earning additional fees to fill swaps on custom AMM curves.

- ◆Integrated with Uniswap v4 hooks, combining lending and automated market-making (AMM) for higher yields and users seeking DeFi composability.

- ◆Allows for JIT (Just-in-Time) liquidity swaps, which refers to borrowing large chunks of an asset to fill a large swap in order to receive the trading fee on that swap.

- ◆If [borrowing interest paid < trading fee earned] → JIT liquidity can happen

- ◆Dynamic hedging: Market makers do delta neutral LPing in DEXs by offsetting the DEX exposure in perpetuals or lending markets.

- ◆Protocol-level liquidity bootstrapping: Instead of paying external LPs to provide liquidity, protocols can create liquidity by borrowing their own tokens and repaying with treasury.

$EUL token sink

Only EUL token holders are allowed to participate in Fee Flow auctions — which enable the earning of protocol fees:

- ◆Fees collected from Euler vaults are usually in other asset types: USDC, ETH, cbBTC, etc.

- ◆EUL holders can bid for those assets at their desired discounts

- ◆Highest bidder wins and pays EUL token as the currency to acquire those assets

- ◆The EUL collected is sent to the DAO treasury, which is locked out of circulation until the DAO decides via governance how to use the funds (e.g. burn, distribute, allocate for marketing)

- ◆Any governance, protocol changes or treasury management has to go through EUL holders.

So, why is $EUL mispriced?

1. Euler’s fundamentals have been exponential while token price lags.

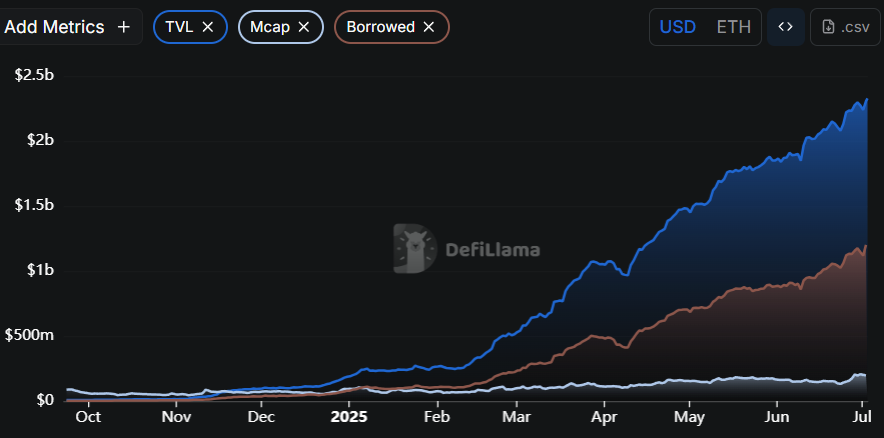

- ◆Since Euler v2 launched in Q4 2024, TVL has grown an astronomical 200x from $10M in Oct 2024 to $2.3B by Jun 2025.

- ◆Total borrows has also grown steadily, indicating effective utilisation of TVL and fee generation on the protocol level.

- ◆EUL market cap has only 4x’d from $50M to $200M in the same period, presumably due several factors, such as the market neglecting older tokens, the protocol’s previous exploit affecting risk-averse buyers and thin on-chain liquidity. EUL is not yet listed on any major T1 exchanges.

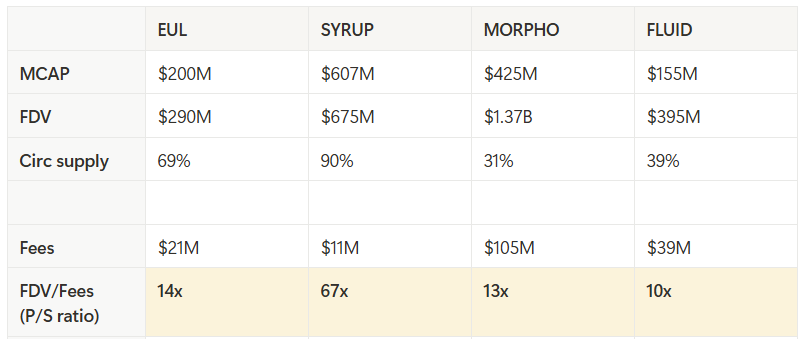

2. EUL trades at 14x P/S ratio with little supply overhang and has the highest 52% borrow rate efficiency.

- ◆EUL trades at $290M FDV while peers are 1.5x ~ 5x richer.

- ◆EUL’s annualised protocol fees ($21M) are 2x larger than SYRUP ($11M) but is trading at half its valuation.

- ◆Note: Protocol fees are used here for simplicity. It is calculated as total interest paid by borrowers with loans, and not necessarily fees that directly benefit token holders.

- ◆EUL’s P/S ratio (indicated here as FDV/Fees) is in line with MORPHO and FLUID, but the latter two suffer from huge supply overhang from monthly token unlocks or incentive emissions.

- ◆EUL supply is 69% circulated as investors and team tokens are largely unlocked while MORPHO and FLUID are newer protocols.

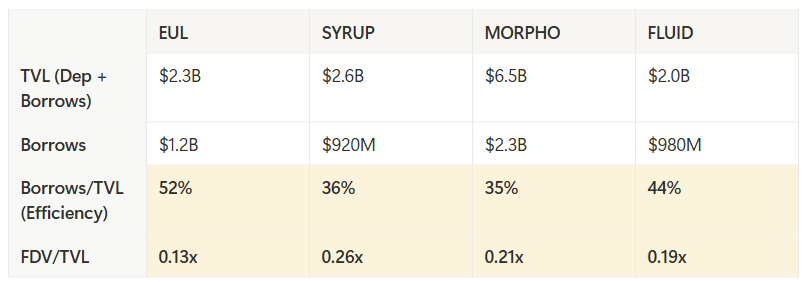

- ◆One of the most important metrics for a lending protocol is Total Borrows, which assesses how effective a money market is at growing its loan book and thus, net interest margins.

- ◆EUL ranks top in terms of generating loans against its total TVL — recording a 52% borrow rate efficiency vs. industry peers ranging 35~44%.

- ◆EUL is the most undervalued when comparing FDV/TVL ratios — 0.13x which gives a minimum 2x room for growth to match SYRUP’s ratio, ceteris paribus.

3. EUL’s setup mirrors trajectories seen in recent breakout tokens like SYRUP

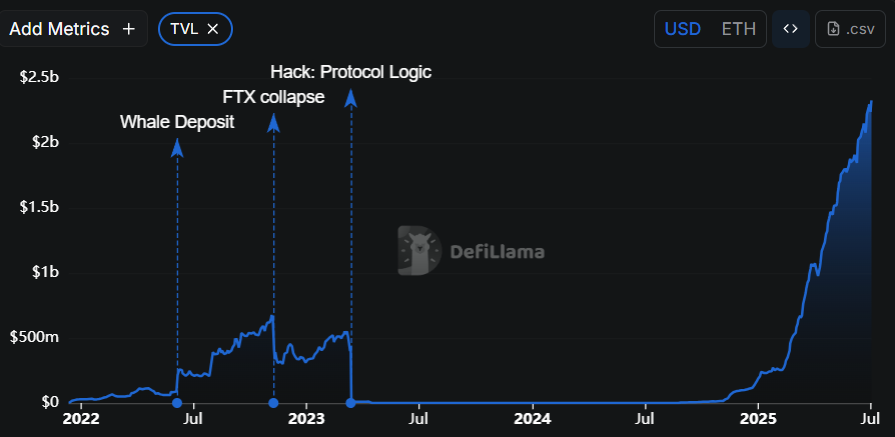

SYRUP is one of the best performing tokens YTD. In hindsight, there was a period to capture its token upside had its fundamentals been studied closely.

Refer to the image below on SYRUP figures:

- ◆Throughout Q1 2025, there was a large divergence between TVL growth and token price.

- ◆TVL grew steadily: $500M → $800M (green arrow)

- ◆Token price dwindled downwards: $0.30 → $0.10 (red arrow)

- ◆The yellow circled area indicates SYRUP’s lows, despite ATH fundamentals, before the market proceeded to rerate SYRUP by 6x.

A similar pattern can be observed in Euler’s surging fundamentals vs. muted token price.

- ◆Euler’s TVL grew tremendously from $10M → $2.3B (200x)

- ◆Token price in the same period went from $3 → $10 (3.3x)

- ◆MCAP: $50M → $200M (circulating supply increased over time)

- ◆FDV: $80M → $272M

- ◆The circled yellow area mimics a trajectory similar to SYRUP before its violent repricing.

What is expected to drive $EUL’s re-rating?

1/ The market beginning to notice EulerSwap’s potential.

EulerSwap is a newly-launched DEX built within Euler’s lending infrastructure.

When a liquidity provider (LP) supplies assets to a lending market, those assets are deposited into Euler vaults — and the same capital can:

- ◆Earn lending yield

- ◆Be used as collateral to borrow other assets

- ◆Double-down as liquidity on the DEX to earn swap fees

In just 2 weeks of launch:

- ◆EulerSwap achieved ~$700M cumulative trading volume (h/t Dune by 0xpibs)

- ◆Based on last 7D trading volumes ($500M), it would be ranked top 15 DEX above Lifinity on SOL, Bluefin on SUI, QuickSwap and Maverick Protocol across multiple chains — all of which have been around for years.

- ◆Peak daily volumes were $90M in recent days → will be exponential as team scales this product

- ◆EulerSwap is also a highly capital efficient DEX, recording >8x in total swap volume size against only $58M in available liquidity.

2/ Institutional adoption of Euler’s modular architecture expediting global recognition.

On 15 May 2025, BlackRock’s BUIDL fund launched its first direct DeFi protocol integration with Euler on Avalanche.

- ◆What it means: BlackRock’s $3 billion tokenised treasury fund introduced sBUIDL, a composable ERC-20 token, enabling DeFi integration.

- ◆Euler integration: sBUIDL is useable as collateral on Euler on Avalanche, to borrow other crypto assets like USDC or AUSD, while earning AVAX incentives and BUIDL’s underlying treasury yield.

- ◆Technical support: Integration curated by Re7 Labs, with Chainlink data feeds ensuring pricing reliability.

- ◆Why it matters: a huge credibility boost for Euler as it marks itself as the first DeFi product to integrate with BlackRock’s BUIDL.

- ◆The bigger picture: a milestone for institutional-grade DeFi, enabling RWAs like money market funds to interact with permissionless protocols — with Euler establishing itself as the first-mover.

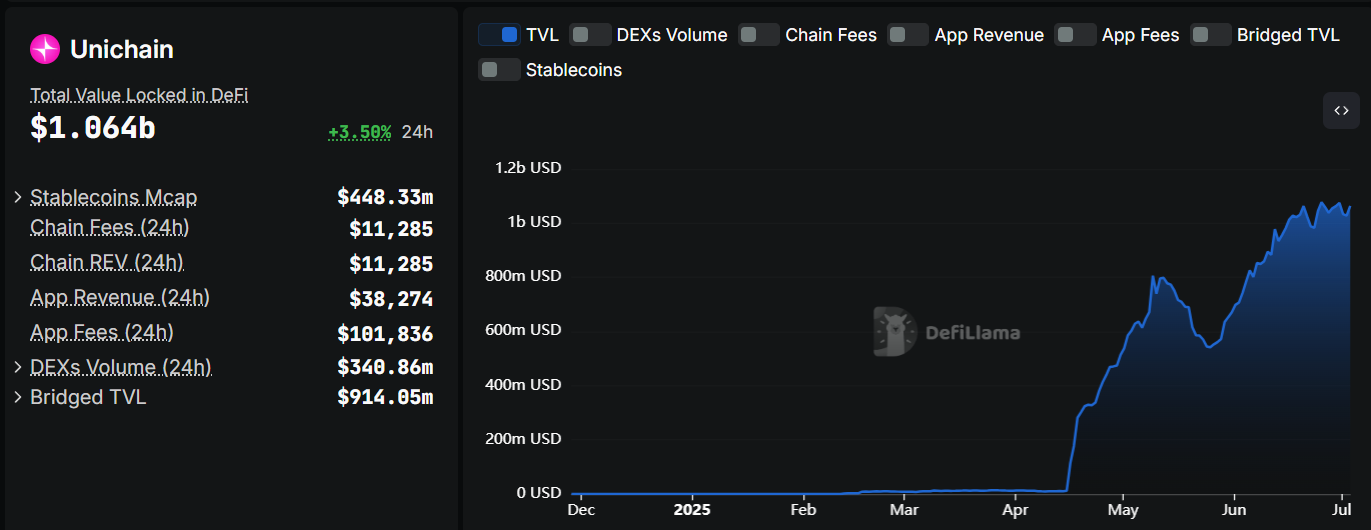

3/ Proxy trade for Unichain season

Unichain’s TVL is gradually creeping up, having grown 100x in 3 months to cross $1B TVL recently. This has drawn market attention and naturally, investor appetite for exposure to the ecosystem.

Euler is the top-ranked protocol on Unichain by TVL and Fees, placing itself as the most direct and liquid proxy trade to an emerging Unichain season.

Euler dominates as the primary DeFi sink on Unichain (it is also built on Uniswap v4 hooks), and there are few other tokens tied meaningfully to Unichain’s growth. EUL could become the market’s preferred way to express bullish bets on the chain’s continued adoption.

4/ Similar characteristics to PENDLE and SYRUP prior to their explosive growths.

- ◆Both PENDLE and SYRUP were products that struggled last cycle (2021-23), but were backed by stellar teams who worked hard to pivot, rebrand and eventually find huge PMF.

- ◆Investors are fully unlocked and most have sold.

- ◆Only originally listed on DEXs before being eventually picked up by Binance for spot listing — which supercharged their product and token’s visibility.

PENDLE — listed Jul ‘23

- ◆FDV: $245M (pre-listing) → $1.1B (now) >> 4.5x

- ◆TVL: $125M (pre-listing) → $4.9B (now)

SYRUP — listed May ‘25

- ◆FDV: $210M (pre-listing) → $700M (now) >> 3.3x

- ◆TVL: $1.3B (pre-listing) → $2.6B (now)

EUL has similar dynamics to PENDLE and SYRUP which may be attractive to new buyers and CEXs.

✅ Strong team that overcame hurdles from last cycle and pivoted to achieve commendable traction

✅ Investors fully unlocked and majority exited positions early on

✅ Current FDV similar to PENDLE and SYRUP prior to their listings, and EUL is not yet listed on any major CEX

- ◆FDV: $290M (pre-listing) → ?

- ◆TVL: $2.3B (pre-listing) → ?

Conclusion

Euler stands out as one of the most fundamentally sound and undervalued assets in DeFi today. Its 200x TVL growth, robust lending metrics, and recent expansion into DEX infrastructure via EulerSwap position it as a multi-pronged protocol with strong product-market fit.

As the market begins to reprice quality and narratives shift toward institutions favouring fundamentals, EUL’s setup mirrors the early phases of breakout tokens like PENDLE and SYRUP — no major CEX listings, minimal supply overhang, and early signs of institutional adoption.

EUL presents a compelling opportunity to accumulate ahead of potential rerating catalysts.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

11

0